{kind=link}

If you’ve collected security of your property and you may you’d like to have flexible the means to access obtain an enormous amount of cash, after that an effective HELOC is a choice for your.

HELOCs can be used for a myriad of expenditures, particularly lingering home improvements or any other opportunities, or can even be used as an emergency need financing. Because they’re secure by your family, you might be capable accessibility more cash at lower notice costs than just that have a charge card otherwise consumer loan. In lieu of with an excellent HELoan, that’s produced given that a single higher lump sum in advance, you have to pay attract on what you draw from your own HELOC, and actually prefer to create attention-only costs? on the first 10 years of your HELOC’s lifetime.

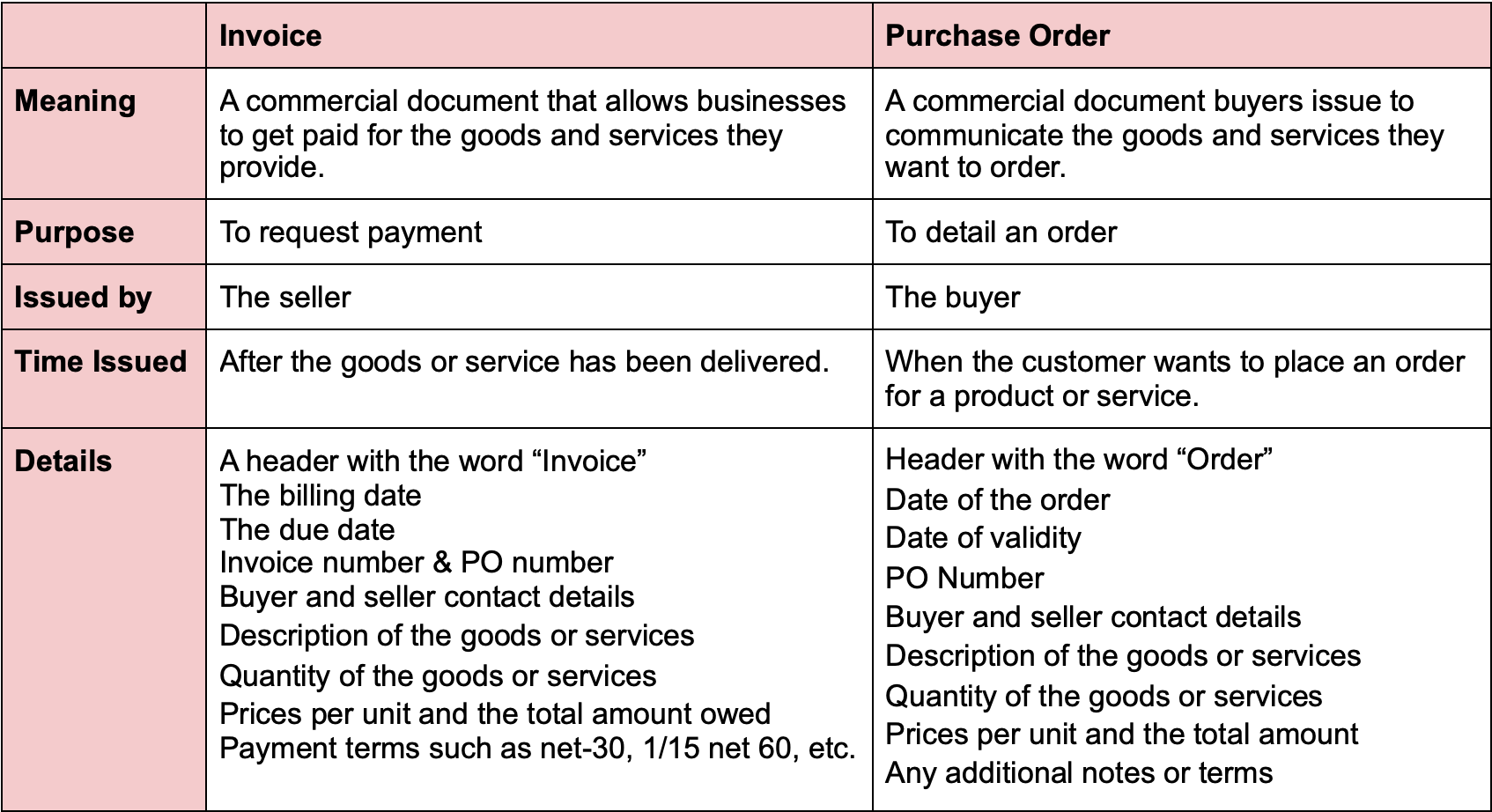

HELOC against HELoan: What is the change?

An effective HELOC are a personal line of credit as possible draw into the when getting a particular mark months (always 10 years), and good HELoan is actually a loan you remove inside the one lump sum initial.

Each other HELOCs and HELoans are financing selection that enable you to borrow against equity which you have made in your home, that give usage of more income having lower interest levels than simply signature loans otherwise credits notes can offer. HELOCs typically americash loans Atmore have changeable APRs, meaning that their attention pricing depend on the top Rates due to the fact authored on Wall surface Road Journal and they are planning change-over go out. It indicates your monthly obligations is consistent, which makes it easier and make a funds-and stick to it.

For more information on the differences ranging from a good HELOC and you will a great HELoan and exactly how you could potentially favor if a person of those was the best option to you personally, see Prosper’s prominent blog site post one holiday breaks everything down: HELOC against HELoan: What is the distinction?

What the results are if i don’t use my personal HELOC?

HELOCs typically have conditions in regards to the minimal you need to mark initially, however, past one, you usually never ever need mark HELOC fund you don’t need * .

Contemplate, that you do not shell out attract to your people HELOC funds that you do not use. Additionally, you could prefer to pay back your balance, accumulated attract, and charges anytime.

Just how long is actually an effective HELOC mark period?

Through the a good HELOC’s draw period, you could draw however much you prefer * to the restrict line of credit, pay it back, and mark once again. It’s also possible to like to create attention-only monthly payments? and hold back until the latest fees several months to repay the principal your borrowed.

Can also be a home security credit line be refinanced?

Property guarantee line of credit are refinanced any kind of time time, however, there could be particular limitations based your area plus lender’s conditions.

In addition, there can be always zero prepayment penalty getting closing-out an effective HELOC. One thing to recall is that you only pay notice to the dollars you use, when you would like you pays your balance right down to $0, you can keep the fresh new range open to include in the long term if you need it at a later time.

Exactly what do I take advantage of my HELOC fund to possess?

HELOCs are used for home improvements, debt consolidating, paying down a home loan, major commands (products, vehicles, RVs, boats, an such like.), plus various expenses. *** For more during these popular uses from HELOCs, look for Prosper’s e-book, 4 How to use a home Equity Credit line.

How try a beneficial HELOC paid?

It is possible to pay-off good HELOC comparable ways you will do a charge card, but you can choose simply how much dominating we would like to pay off within the draw months, if you don’t create interest-simply repayments? during that time.